This article, "Analysis of the ACL under ASC 326 – Is Another Banking Crisis Looming?," originally appeared on GAAPDynamics.com.

A GAAP Dynamics Blog Powered by Intelligize®

More often than I’d like to admit, I get a wild hair, go down a rabbit hole, and spend way too much time writing a post about an accounting topic. What can I say? I’m an accounting geek at heart! Case in point: My Alice in Wonderland-inspired post regarding the games some banks were playing by trying to hide unrealized losses in their investments in debt securities by transferring them from available for sale to held to maturity. Well, I’m back at it again, this time analyzing the allowance for credit losses (ACL) calculated under ASC 326 to see if banks have enough reserves, which according to the Fed, “higher reserves put banks in a stronger position to deal with any future deterioration in asset quality.” Do banks have enough reserves to weather the storm of the inevitable recession that everyone says is coming? I’ll cut to the chase. In my opinion, they do not, but I’ll let you decide for yourselves after reading this post.

The genesis of this post came when Vicky and I were teaching a week-long training program for a Top 25 bank. It’s a great training program and one of my favorites because we are helping the bank’s new hires, recent college graduates, understand the accounting and reporting considerations for banks using the bank’s own financial statements, as well as the financial statements of their competitors. Through this hands-on review, participants really begin to understand this new industry in which they’ve decided to start their careers. We’ve done this training program for this bank for many years to great reviews!

When teaching them about the allowance for credit losses (ACL) calculated under the new CECL model set out in ASC 326, we were reviewing the related disclosures contained within the financial statements and doing some analysis. Specifically, I asked them to review the amount of the ACL as a percentage of total loans held for investment. I wanted to see how their “reserves” for total loans stacked up against each other and whether that ratio was increasing or decreasing from prior periods. Each group was assigned one of the following banks:

- Truist

- Fifth Third

- Regions

- Zions

- M&T Bank

- PNC Financial

- KeyCorp

- Huntington

- Citizens

- Comerica

The percentage of ACL to total loans went down in 2022 from 2021 for seven of the ten banks. That really didn’t surprise me. The ACL is such an entity-specific estimate that depends on many factors. However, I was shocked by the percentages that were being presented, ranging from 1.12% to 1.81%. Why? Because I am old enough to have lived through the Great Recession beginning in the fourth quarter of 2007, the most severe worldwide economic crisis since the Great Depression of 1929. And these ratios seemed awfully low!

Back in 2008/09, when dissecting the crisis and why it happened, I remembered teaching participants how the percentage of allowance for loan and lease losses (ALLL), which is what we used to call it prior to the adoption of ASC 326, to total loans was at an all-time low for the industry just before the crisis hit. And my fear was that we were approaching these levels again. However, I needed data to support my hypothesis that the ACL for banks is approaching levels not seen since the Great Recession.

In my previously mentioned post, I spent days on the web downloading the individual annual reports of banks, reviewing them, pulling out the appropriate figures, and inputting them to an Excel document. It was a labor of love, but, in hindsight, completely unnecessary because there are technological solutions in the marketplace, like Intelligize®. One of the perks of our strategic alliance with Intelligize® is that they gave us access to their powerful web-based research platform, allowing me to do the analysis for this post much faster.

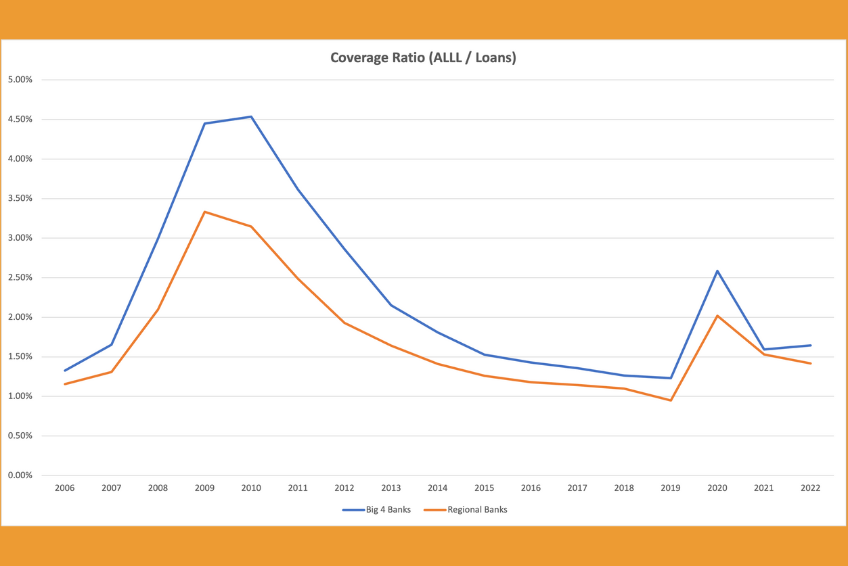

So, here’s what I did. Using Intelligize, I pulled the annual reports from 2006 through 2022 for those ten banks plus the four largest (JPMorganChase, Bank of America, Citigroup, and Wells Fargo). For each bank and each year, I then got the ACL (or ALLL) and the total loans held for investment (this is important because loans held for sale are not included in the allowance calculation) and calculated the ratio. Here’s a chart documenting my results:

This ratio for all banks in the analysis was 1.59% at the end of 2007 and was 1.58% at the end of 2022. As you can see in the chart, for the “big” banks, this ratio was 1.65% in 2007 and was at 1.64% in 2022. The regional banks included in my analysis were a bit better. The ratio in 2007 was 1.31%, while it was 1.42% in 2022.

So, my hypothesis was correct! The ratio of the allowance to total loans held for investment is nearly the same level as it was just before the Great Recession. However, and here’s the kicker, the calculation is different, which, in my opinion, makes this issue even worse.

You see under the “old” model for calculating the ALLL, estimates were calculated under an “incurred loss” model. This means a loss had to have been incurred by the reporting date for an allowance to have been recorded. However, under ASC 326, the CECL model is an “expected loss” model, meaning that we must put up an allowance for the estimated losses over the contractual life of the loans upon origination. This estimate of expected losses needs to consider historical losses, updated for current conditions and reasonable and supportable forecasts.

All things being equal, you would expect that the ACL calculated under ASC 326 would be higher than the ALLL calculated under previous GAAP. In fact, my analysis proves this as EVERY SINGLE ONE of the banks in my analysis saw dramatic increases in the ACL (as a percentage of total loans held for investment) upon adopting the CECL model in 2020, some nearly tripling their coverage. To be fair, the balance of their ACLs was woefully low prior to the adoption of CECL, with some of the ratios dipping well below 1%.

However, wouldn’t you expect that today’s ACL (calculated under an “expected loss” model), especially given all the turmoil out there, would be higher than the ALLL (calculated under an “incurred loss” model) prior to the Great Recession?

I would, which is why I wrote this post!

Hopefully, the banks can support their ACL estimate and auditors are properly challenging this management estimate, which certainly rises to the level of a critical audit matter (CAM). According to the OCC, “ACLs should be well documented, with clear explanations of the supporting analyses and rationale. Maintaining, analyzing, supporting, and documenting appropriate ACLs and PCLs (provision for credit losses) in accordance with GAAP is consistent with sound and safe banking practices. Internal control systems for the ACL estimation processes should provide reasonable assurance regarding the relevance, reliability, and integrity of data and other information used in estimating expected credit losses.”

Let me know what you think. Are my worries founded or am I being a Chicken Little?

About GAAP Dynamics

We’re a DIFFERENT type of accounting training firm. We don’t think of training as a “tick the box” exercise, but rather an opportunity to empower your people to help them make the right decisions at the right time. Whether it’s U.S. GAAP training, IFRS training, or audit training, we’ve helped thousands of professionals since 2001. Our clients include some of the largest accounting firms and companies in the world. As lifelong learners, we believe training is important. As CPAs, we believe great training is vital to doing your job well and maintaining the public trust. We want to help you understand complex accounting matters and we believe you deserve the best training in the world, regardless of whether you work for a large, multinational company or a small, regional accounting firm. We passionately create high-quality training that we would want to take. This means it is accurate, relevant, engaging, visually appealing, and fun. That’s our brand promise. Want to learn more about how GAAP Dynamics can help you? Let’s talk!

Disclaimer

This post is published to spread the love of GAAP and provided for informational purposes only. Although we are CPAs and have made every effort to ensure the factual accuracy of the post as of the date it was published, we are not responsible for your ultimate compliance with accounting or auditing standards and you agree not to hold us responsible for such. In addition, we take no responsibility for updating old posts, but may do so from time to time.