This article, "ICYMI—Applying the New Accounting Guidance for Contributions," originally appeared on CPAJournal.com.

In Brief

Not-for-profit organizations receive financial donations as a matter of course, but the accounting for that revenue depends on whether the transaction is classified as a contribution or an exchange, and the distinction between the two is not always easy to make. FASB has recently released new guidance on how to determine whether a transaction is a contribution or an exchange. The authors explain how the new guidance works and provide examples of how nonprofits should apply it when recognizing revenue from these transactions.

* * *

In June 2018, FASB issued Accounting Standards Update (ASU) 2018-08, Clarifying the Scope and Accounting Guidance for Contributions Received and Contributions Made, with the stated purpose of providing guidance in evaluating whether transactions should be accounted for as contributions or exchanges. In addition, the update introduces the concept of barriers in providing additional guidance on identifying conditions that would preclude the recognition of a contribution as revenue.

ASU 2018-08 changes the reasoning process behind classification of transactions, the nuances of which may affect the timing of revenue recognition. Contributions and exchanges are governed by different accounting pronouncements, and therefore may be recognized in different accounting periods and require different disclosures.

FASB expects the new guidance on barriers to result in more contributions being classified as conditional; conditional contributions will not be recognized as revenue and expense until those barriers are overcome. As a practical matter, ASU 2018-08 will not change the timing of the recognition of revenue and expenses in many instances, but reporting entities must follow the required process. In any event, the ultimate amount of revenue and expense recognized over time will be the same regardless of the transaction’s classification.

ASU 2018-08 applies to all entities that receive or make contributions, including both business and not-for-profit entities (NFPs). The update is expected to have a greater impact on NFPs because contributions are a significant source of their revenue.

Public business entities or NFPs that are conduit bond obligors for securities quoted on an exchange should apply ASU 2018-08 for fiscal years beginning after June 15, 2018. All other entities should apply the update in fiscal years beginning after December 15, 2018.

This article outlines the basic principles of ASU 2018-08 and presents examples of application by NFP recipients of contributions. It presumes the NFPs have adopted ASU 2016-14, Presentation of Financial Statements of Not-for-Profit Entities.

Basic Concepts

ASU 2018-08 defines a contribution as “an unconditional transfer of cash or other assets, as well as unconditional promises to give, to an entity, or a reduction, settlement, or cancellation of its liabilities in a voluntary nonreciprocal transfer by another entity acting other than as an owner.” Thus, the transfer of assets or settlement of liabilities must be both voluntary and nonreciprocal in order to be a contribution. These characteristics distinguish contributions from exchanges, which are reciprocal transfers in which each party receives and sacrifices approximate commensurate value. These characteristics also distinguish contributions from involuntary nonreciprocal transfers, such as impositions of taxes or legal judgments, fines, and thefts. The definition also excludes transactions with owners, such as investments by owners and distributions to owners.

Under ASU 2018-08, any type of entity can be a resource provider or recipient. For example, a provider may be a government agency, a foundation, a corporation, or another entity. A recipient may be either a for-profit business or an NFP.

In applying ASU 2018-08, all recipients of contributions should perform the following procedures on each agreement:

- Determine whether the transaction is an exchange or contribution.

- If the transaction is a contribution, identify any donor-imposed conditions or restrictions regarding its use.

- Distinguish between barriers and donor-imposed restrictions.

- Conclude that all conditions are resolved prior to recognizing the contribution as revenue.

Both providers and recipients are required to use the same criteria in determining whether transfers are contributions or exchanges and whether any contributions are conditional or unconditional. Although symmetry between providers and recipients is envisioned, ASU 2018-08 does not require that both parties record contributions provided and received in the same period and in the same amounts. For example, providers are not required to obtain information on or assess the recipients’ conclusions on overcoming any barriers.

ASU 2018-08 provides “indicators” rather than bright lines in distinguishing a contribution from an exchange.

Pursuant to Accounting Standards Codification (ASC) 720-25, providers should recognize unconditional contributions as expenses in the period made. Providers should defer recognizing any conditional contributions as expenses until all conditions are satisfied. As with revenue recognition, a contribution expense should not be recognized based on an expectation that the recipient is likely to satisfy the condition.

Exchanges vs. Contributions

NFPs apply different accounting pronouncements to contributions and exchanges. Contributions are within the scope of ASC Topic 958, “Not-for-Profit Entities.” Exchanges are subject to other guidance, such as ASC Topic 606, “Revenue from Contracts with Customers.” The application of these different rules will affect when revenue is recognized; unconditional contributions are recognized in the period when either assets or specified assets are received or promised, while exchanges are recognized as revenue when performance obligations are satisfied.

ASU 2018-08 provides “indicators” rather than bright lines in distinguishing a contribution from an exchange. NFPs should evaluate the terms of each agreement by considering the following indicators in order to determine whether the transaction is predominately a contribution or an exchange:

- The expressed intent of both the recipient and the provider to exchange resources for goods or services that are of commensurate value is indicative of an exchange.

- The provider having full discretion in determining the amount of the transferred assets is indicative of a contribution. Both the recipient and the provider agreeing on the amount of assets transferred in exchange for goods and services is indicative of an exchange.

- The provider is not synonymous with the general public and, therefore, does not receive commensurate value when it transfers funds to another entity for the purpose of providing a benefit to the public.

- A provider does not necessarily receive commensurate value when it transfers funds for activities consistent with its mission or obtaining any positive sentiment from acting as a donor.

- The extent of penalties assessed on the recipient for failure to comply with the terms of the agreement may affect the classification of a transaction as either a contribution or an exchange. Penalties limited to the delivery of assets or services already provided and the return of the unspent amount are generally indicative of a contribution. Penalties in excess of the amount of assets transferred by the provider generally indicate that the transaction is an exchange.

In addition, the following transactions and activities are not generally contributions:

- Transfers of assets that are in substance purchases of goods or services

- Transfers of assets in which the reporting entity acts as an agent, trustee, or intermediary

- Tax exemptions, tax incentives, or tax abatements

- Transfers of assets from government entities to business entities

- Transfers of assets that are part of an existing exchange between a recipient and an identified customer, such as payments made in Medicare and Medicaid programs; provisions of healthcare or education services by a government for its employees; and federal, state, or local government tuition assistance programs.

Recipients need to understand the terms of each of their contribution agreements, because none of the indicators listed above definitively distinguish a contribution from an exchange. For example, the sale of goods or services at significantly below-market prices may be deemed to be a partial contribution. Such contributions are measured at the difference between the fair value of the products provided or services performed and the consideration received.

The following are examples of different NFPs applying the above guidance.

Social Program Provider—Exchange Incorporating Indicators of Contributions

Omega Agency provides residential, rehabilitation, and day programs to individuals with disabilities and their families. Programs are funded by state government grants, Social Security Administration (SSA) and Medicaid fees, customer payments, and contributions. SSA and Medicaid fees are based on the number of qualified individuals and days of service. The state bases the amounts of its grants on costs it deems allowable. Omega submits a report listing allowable costs proposed for the upcoming year, which the state reviews in accordance with its regulations. Based on its review and any of its required revisions, the state authorizes the amounts of its grants.

In determining whether the state grants and the SSA and Medicaid fees are exchanges or contributions, Omega applies the terms of the funding agreements to the indicators noted above. At first glance, it would appear that these grants and fees are contributions. The providers appear to have full discretion in determining the amount of the transferred assets, and also determine the eligibility of individuals to participate in the various programs and the type and amounts of costs that are allowable. Finally, ASU 2018-08 specifically asserts that any public benefit derived from this funding is not an indicator of an exchange.

ASU 2018-08 also specifically asserts that transfers of assets that are part of an existing exchange between a recipient and an identified customer are generally not contributions.

ASU 2018-08 also specifically asserts, however, that transfers of assets that are part of an existing exchange between a recipient and an identified customer are generally not contributions. In evaluating the agreements, Omega determines that it is providing services to specified individuals who are receiving a benefit of commensurate value. Payments made by the state, SSA, and Medicaid are third-party funding arrangements of this transaction between the agency and specified individuals, which are analogous to health insurance contracts. Accordingly, this is an exchange by definition.

In this instance, Omega applies the applicable guidance, such as Topic 606 or the AICPA Audit and Accounting Guide, Revenue Recognition, to the underlying transaction with the customers and accounts for the payments from the third parties as payments on behalf of those customers.

Social Advocate—Distinguishing Between Contributions and Exchanges

ABC Foundation is dedicated to achieving gender equality and empowerment. Every year, the network holds an advocacy event that includes performances by major entertainers. This event generates contributions and sponsorships by major corporations. ABC engaged in the following transactions during the year ending December 31, 2019.

Contribution from foundation.

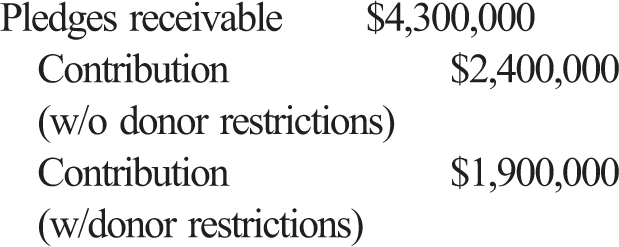

On March 5, 2019, Alpha Network (Alpha) pledged $4.3 million to ABC in response to appeals associated with the event. The purpose of this pledge was to fund activities consistent with the network’s mission. Pursuant to the pledge agreement, Alpha provided $2.4 million within one week of the grant being signed and promised to provide $1.25 million on March 1, 2020, and $650,000 on March 1, 2021. The 2020 and 2021 payments will only be made after the network provides progress reports prepared in accordance with the agreement. The agreement anticipates that these progress reports will be submitted no later than February 1 of the applicable year.

This pledge meets the definition of a contribution in that it is an unconditional transfer of cash that is both voluntary and nonreciprocal. By definition, any societal benefit received by Alpha is not considered to be of commensurate value.

As discussed below, the progress reports do not create a barrier that would defer revenue recognition; ASU 2018-08 considers these to be administrative matters that do not rise to the level of a barrier. The payments due on March 1, 2020, and March 1, 2021, however, are subject to a time restriction because the donor does not make these funds available until those dates. As a consequence, ABC Foundation would post the following journal entry on March 5, 2019:

Corporate sponsor—basic agreement.

Bravo Corporation (Bravo), a manufacturer of industrial products, pledged $750,000 for the event. The pledge document required ABC to perform specific activities, all of which are consistent with its normal operations. ABC agreed to identify Bravo as a sponsor of the event on its website and in other communications and to permit Bravo to publicize its participation in its corporate advertising. Bravo did not receive any other benefits, such as free tickets to the event, as a result of this sponsorship.

ASU 2018-08 asserts that any positive sentiment from acting as a donor does not constitute commensurate value received by the provider for purposes of determining whether the transfer of assets is a contribution or an exchange. Thus, Bravo’s transfer of cash to the ABC event is not an exchange, because Bravo’s sole benefit is good publicity. In the absence of any donor-imposed restrictions, ABC would account for the entire grant as a contribution without donor restrictions.

Corporate sponsor—complex agreement.

Charlie Corporation (Charlie), a manufacturer of consumer products, pledged $3.5 million for the event. As with Bravo, the pledge document required ABC to perform specific activities, all of which are consistent with its normal operations. It agreed to identify Charlie as a sponsor of the event on its website and in other communications and to permit Charlie to publicize its participation in its corporate advertising.

Charlie, however, imposed the following additional requirements:

- If a third-party competitor proposes to sponsor the event, Charlie has the right to revise the agreement to include identical or more favorable terms.

- Charlie has the right to display its name and logo on all promotional material regarding the event.

- Charlie has dedicated space at the event to present its name and products.

- Charlie may gift its products to the performing entertainers and certain influential people.

- ABC Foundation will announce Charlie’s commitment to its mission on stage during the event.

- Charlie will have the opportunity to present event content along with its corporate name and logo, both during and after the event.

- Remedies to breaches are specified by the agreement.

Any positive sentiment from acting as a donor does not constitute commensurate value received by the provider for purposes of determining whether the transfer of assets is a contribution or an exchange.

One indicator in concluding whether a transfer of assets is a contribution or an exchange is that the positive sentiment from acting as a donor does not constitute commensurate value received by the resource provider. This indicator was the basis for concluding the contribution from Bravo was not an exchange. Charlie, however, receives more than positive sentiment, such as greater visibility than Bravo and the means to promote itself and its products. Accordingly, Charlie is receiving commensurate value as the provider. ABC Foundation would thus apply Topic 606 in accounting for this transaction.

In applying Topic 606, the network must determine whether Charlie’s right to present event content along with its corporate name and logo during the event is a separate performance obligation from those rights after the event. Revenue allocated to a performance obligation satisfied after the event must be recognized over the expected period of benefit. In this case, ABC was not obligated to perform any further activities in providing this benefit. Accordingly, ABC recognized this entire transaction obligation on the date of the event and recorded the following journal entry:

A theoretical question is whether the fair value of the benefits received by Charlie is less than the $3.5 million grant. As discussed below, this circumstance would result in bifurcating the grant into an exchange (publicity) and contribution (the difference between the fair value of the publicity and total amount provided). Given the described circumstances, this contract would be recognized in the same period regardless of whether it was classified as an exchange or contribution. In addition, the determination of the fair value of publicity is highly subjective. Thus, any allocation between exchange and contribution revenue would provide little benefit.

Council—Partial Contribution with Donor Restrictions

Delta Council coordinates fundraising and other activities with NFPs with similar missions and objectives. Every year, Delta conducts a gala that features dinner and entertainment. During the year ending December 31, 2019, the council receives proceeds of $3.2 million from gala participants and incurs expenses of $700,000.

ASU 2018-08 notes that the exchange of assets or performance of services in exchange for assets of substantially lower value may be deemed to be a partial contribution. Such contribution would be measured at the difference between the fair value of the products provided or services performed and the consideration received. The dinner and entertainment provided during the gala is an exchange in that both the participants and the council receive and sacrifice approximately commensurate value. The exchange would be measured by the cost of the gala ($700,000), which approximates the fair value given the short time period between the council’s incurring the costs and the actual date of the gala. The difference between the fair value of the service and proceeds—$2.5 million—is a contribution. The update does not significantly change the current accounting rules for this transaction.

In the absence of any donor restrictions, the contribution would be classified as without such restrictions; however, if the advertised purpose of the gala is restricted to some purpose, such as a specific research project or capital campaign, the contribution would be classified as with donor restrictions.

Identifying Conditions and Barriers

Many contribution agreements specify obligations of both the provider and recipient. The obligations can take various forms, such as activities consistent with the recipients’ normal operations, donor-imposed restrictions, and donor-imposed conditions. These obligations are subject to different accounting rules and therefore must be properly identified. Contributions funding activities consistent with the recipients’ normal operations are generally classified as contributions without donor restrictions. Donor-imposed conditions and restrictions have a greater effect on financial reporting because they limit the recipients’ use of those assets.

ASU 2018-08 precludes the recognition of a contribution as revenue if the contribution is conditional on events beyond the control of either the resource provider or recipient. A donor-imposed condition exists when it is determinable from the agreement that a recipient is entitled to the contribution only if it has overcome a barrier. A donor-imposed condition must have both—

- one or more barriers that must be overcome before a recipient is entitled to the assets transferred or promised; and

- a right of return to the provider for assets transferred (or for a reduction, settlement, or cancellation of liabilities), or a right of release of the promisor from its obligation to transfer assets (or reduce, settle, or cancel liabilities).

A donor-imposed condition exists when it is determinable from the agreement that a recipient is entitled to the contribution only if it has overcome a barrier.

These criteria are achieved by the contribution agreement specifying that the recipient must meet the stipulations before becoming entitled to the transferred assets. The agreement does not need to specifically refer to a right of return or release from obligation; it only has to be sufficiently clear to support a reasonable conclusion about when a recipient would be entitled to the contribution. Agreements that have donor-imposed restrictions (as opposed to barriers) and a right of return are not conditional.

ASU 2018-08 does not define the term “barrier”; instead, it describes it using indicators. In determining whether an agreement contains a barrier, the recipient should evaluate the terms of each agreement while considering those indicators. Depending on the facts and circumstances, some indicators may be more significant than others, and no single indicator is determinative:

- Measurable performance-related barrier or other measurable barrier. Examples include the achievement of a specified level of service, an identified number of units of output, or a specific outcome, such as a matching requirement.

- Limited discretion by the recipient on the conduct of an activity. Limited discretion of the recipient is more specific than a donor-imposed restriction. Examples of this indicator include requirements to follow specific guidelines about incurring qualifying expenses, hiring specific individuals to conduct the activity, and adhering to a specific protocol.

- Stipulations that are related to the purpose of the agreement. This indicator includes specific requirements, such as a homeless shelter providing a specified number of meals to eligible individuals. It does not include goals or budgets where no penalty is assessed if the recipient fails to achieve them.

Assets received in a conditional contribution should be accounted for as a refundable advance until the conditions have been substantially met or explicitly waived by the donor. Revenue is recognized on the date the condition was met; it is not recognized on the grant date.

ASU 2018-08 does not provide specific guidance in distinguishing barriers from donor-imposed restrictions. Reporting entities are required to use professional judgment in applying the various indicators to the facts and circumstances of each agreement to conclude whether stipulations are conditions or restrictions. A donor-imposed condition places limitations on how an activity is performed by identifying specific individuals to perform the activity, limiting the use of funds to specific activities, or requiring benchmarks that must be met before the barrier is deemed satisfied. In contrast, restrictions limit the use of a contribution to a specific activity or time, but not necessarily to the way the activity is performed. Some conditional contributions may also impose restrictions after the conditions are resolved.

Some agreements contain ambiguous provisions that do not clearly state whether the right to receive or retain a contribution depends on meeting specific stipulations. In these cases, reporting entities should clarify the intent of the contribution with the donor. If the ambiguity cannot be resolved, ASU 2018-08 presumes that any contribution containing stipulations that are not clearly unconditional is conditional. The reporting entity is precluded from performing a probability assessment to conclude whether the reporting entity will fulfill a stipulation. Thus, the mere existence of such stipulations is sufficient to conclude that the agreement contains a barrier.

The absence of any indication of a barrier supports the conclusion that the contribution has no donor-imposed conditions.

The application of ASU 2018-08 requires considerable judgment in assessing facts and circumstances. For example: Omega Agency received grants whose amounts were determined by the state after reviewing an agency report listing allowable costs proposed for the upcoming year. This would appear to limit Omega’s discretion on the conduct of the activity and therefore make the grants conditional. This review, however, takes place before the period in which the grants apply. Because the conditions are met before the agency is entitled to the grants, this indicator has no effect on the recognition of revenue.

In a similar vein, ABC Foundation is required to provide an annual report, which theoretically gives Alpha Network the ability to disallow expenditures and withhold future promised grants. ASU 2018-08 considers provisions that are unrelated to the purpose of the agreement, such as administrative stipulations, as not indicative of a barrier. These administrative stipulations include routine reporting on expenditure of funds or a summary of the recipient’s actions taken to meet the barrier specified in the agreement; ABC thus recognizes the grant as unconditional.

ASU 2018-08 makes the recognition of contributions conceptually consistent with Topic 606.

University—Conditional Grant

Kappa University is conducting a capital campaign to raise funds to replace an obsolete building on campus. An individual donor placed a $6 million contribution restricted to the construction of the new building in an escrow fund. The release of this gift is contingent upon the university obtaining and collecting at least $6 million of other contributions restricted to the construction of the building within six months of the grant date. Kappa University must collect the entire $6 million of matching contributions before the individual’s gift is transferred. The entire gift is returned to the individual if the university does not collect the $6 million in matching contributions. The contribution agreement prohibits a pro rata allocation of the grant. (For example, if the university collects $4.5 million, it is not entitled to 75% of the contribution.)

This contribution is conditional based on a measurable performance-related barrier. Kappa University must actually collect the entire $6 million matching contributions before it recognizes the donor’s gift as contribution revenue.

Conceptual Consistency

ASU 2018-08 makes the recognition of contributions conceptually consistent with Topic 606. Just as Topic 606 requires revenue to be recognized when performance obligations are satisfied, ASU 2018-08 requires contribution revenue to be recognized after conditions are met. The additional guidance in distinguishing contributions from exchanges also relies on an identification of the existence of or lack of performance obligations.

The implementation of ASU 2018-08 will affect different NFPs in various ways, depending on the nature of their sources of revenue. Although the measurement and timing of recognition of certain contributions may not change as a result of this update, NFPs need to apply the process described in the update to their agreements in order to determine the proper accounting.

Marc Taub, CPA is an audit principal at MBAF CPAs LLC, New York, N.Y.

David Hollander, CPA is an audit principal at MBAF, Boca Raton, Fla.

Lisette Rodriguez, CPA is an audit principal at MBAF, Miami, Fla.

Robert A. Dyson, CPA is the director of quality control at MBAF, New York, N.Y., and a member of The CPA Journal Editorial Board.