This article, "The Expanding Use of Non-GAAP Financial Measures," originally appeared on CPAJournal.com.

In Brief

There is a long history of businesses reporting non-GAAP financial measures, often to highlight a change in operating structure or illuminate the impact of a merger or acquisition. But since the 1990s, companies have increasingly used non-GAAP financial measures as a way to adjust earnings in ways that may help investors understand their core business. A lack of guidance, however, has opened the door to potentially misleading financial reporting, leading the SEC to get more involved. The authors review the current problems with non-GAAP financial measures so that auditors can help ensure that management not run afoul of regulatory scrutiny.

Despite the recent attention and scrutiny by regulators and standards setters, non-GAAP financial measures are not a recent phenomenon. Initially, non-GAAP measures highlighted material changes in a company’s operating structure or accounting method. For example, a company might have presented pro forma historical/future non-GAAP financial statements if it had engaged in a significant merger or acquisition, either to allow for historical comparability or to detail the expected future performance of the company following the transaction.

The use of non-GAAP financial measures began to change in the 1990s, when companies began providing non-GAAP earnings and disclosures that they argued provided investors with improved insight into the company’s ongoing core business earnings. When presenting non-GAAP information, companies have significant discretion in adjusting GAAP-based earnings by excluding noncore expense items or including revenue items not recognized under GAAP rules. In response, the SEC continues to evaluate whether companies are using their discretion in non-GAAP earnings reporting to inform or mislead investors. This article details the SEC’s historical treatment of non-GAAP measures, reviews problems associated with non-GAAP measures, and provides ways that a company’s auditors, accountants, executives, and audit committee members can reduce the probability of a non-GAAP disclosure being deemed misleading.

SEC Interest in Non-GAAP Measures

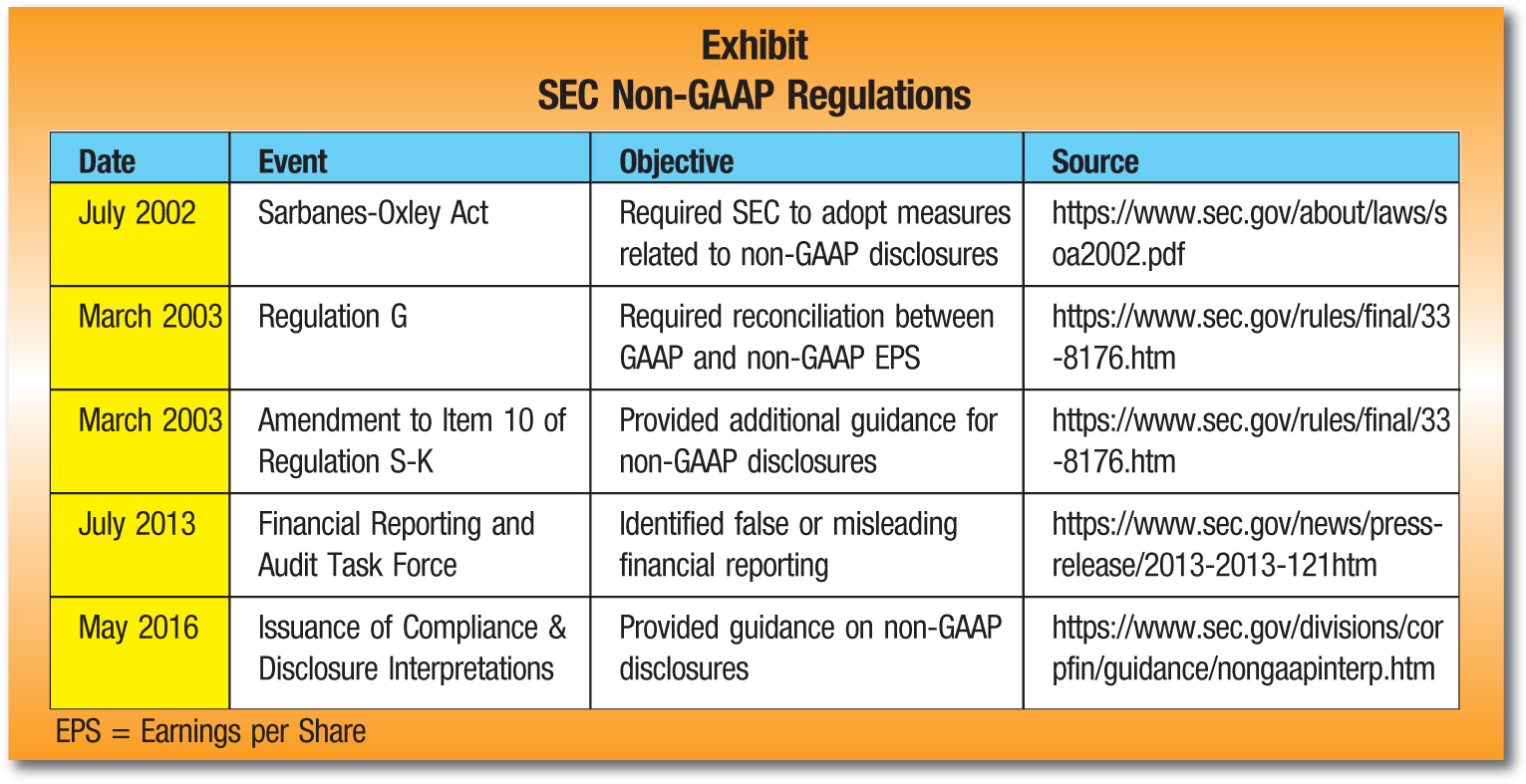

In 2000, SEC Chief Accountant Lynn Turner referred to non-GAAP earnings as reporting “everything but the bad stuff.” Turner provided several examples of companies presenting non-GAAP earnings that were misleading to investors. Non-GAAP reporting has become even more prevalent since Mr. Turner’s speech, resulting in regulatory responses by the SEC. A brief overview of SEC non-GAAP regulations and links for further information are provided in the Exhibit.

Exhibit

SEC Non-GAAP Regulations

The Sarbanes-Oxley Act of 2002 required the SEC to adopt measures to minimize misleading non-GAAP reporting. In response, the SEC adopted Regulation G and amended Item 10 of Regulation S–K. Regulation G and the amendment to Item 10 require companies to prepare a reconciliation between the non-GAAP measure and the most similar GAAP measure, and to refrain from excluding nonrecurring or unusual expenses from non-GAAP measures if the expenses are reasonably likely to recur. The public disclosures covered by Regulation G include, but are not limited to, conference calls, PowerPoint presentations, and press releases. If the format of a disclosure is not conducive to providing a reconciliation, companies can place the reconciliation on their website and are required to reference the website reconciliation in the disclosure.

The regulatory concern over the use of non-GAAP measures did not end after the passage of Regulation G. In 2010, Howard Scheck, former chief accountant of the SEC’s Division of Enforcement, called non-GAAP exclusions a “fraud risk factor.” In July 2013, the SEC created the Financial Reporting and Audit Task Force, with a primary focus of the analysis of companies’ use of non-GAAP disclosures; five months later, David Woodcock, chairman of the task force, explicitly stated that it was investigating non-GAAP disclosures. In 2015, SEC Chair Mary Jo White cautioned preparers of financial statements not to use non-GAAP disclosures in an attempt to improve the appearance of a company’s financial performance. White also highlighted the SEC’s concern with non-GAAP reporting in 2016 when she stated that the use of non-GAAP expense exclusions is “something that we are really looking at—whether we need to rein that in a bit even by regulation.”

In a 2016 speech at the U.S. Chamber of Commerce’s 10th Annual Capital Markets Summit, White suggested that the reporting and presentation of non-GAAP measures concerned the SEC. While acknowledging that non-GAAP measures may provide information to investors, the SEC was concerned that non-GAAP numbers were more favorable with respect to the company’s performance and financial health when compared to GAAP-based numbers. At the 2016 Baruch Financial Reporting Conference, SEC Deputy Chief Accountant Wesley Bricker and Chief Accountant of the Division of Corporation Finance Mark Kronforst warned against the inappropriate use of non-GAAP financial measures and explicitly stated that companies presenting an adjusted revenue number would receive a comment letter. Later that year, the SEC issued additional guidance in a set of Compliance and Disclosure Interpretations (C&DI).

In its 2016 SEC Comments and Trends, Ernst & Young (EY) noted that 18% of comment letters issued for the years ending June 30, 2015 and 2016, related to non-GAAP reporting. In the same document, EY noted that non-GAAP measures increased from the fourth most common reason for the issuance of a comment letter in 2015 to the second most common reason in 2016.

Companies primarily distribute non-GAAP information through press releases and conference calls. Because there can be a tremendous amount of leeway in the content and format of these distributions, it is important for the company’s management team, board of directors, audit committee, and auditors to be aware of the ways the SEC considers non-GAAP disclosures to be misleading. In addition, it is essential to emphasize that auditors do not opine on whether non-GAAP measures are more descriptive of core business performance or whether the adjustments are appropriate. In a 2018 discussion, Bricker stated that audit committees should actively review non-GAAP disclosures to minimize the possibility of a company presenting misleading non-GAAP information.

Non-GAAP measures are not unique to the United States. In fact, the IASB is currently developing standards that address the presentation of non-GAAP measures internationally, to be called “Alternative Performance Measures.” There are likely to be significant changes forthcoming for companies reporting under International Financial Reporting Standards (IFRS).

Reporting Non-GAAP Earnings

According to the SEC, a non-GAAP financial measure excludes or includes financial data that is included or excluded in the most comparable GAAP measures. If management believes that publicly disclosing a non-GAAP measure will be beneficial to investors, it must explain why the non-GAAP number provides a better performance measure than the GAAP number and provide a detailed reconciliation between the non-GAAP and most comparable GAAP numbers. If the non-GAAP measure is disclosed orally—for example, during the company’s annual shareholder conference call—the company is required to present a reconciliation or make the reconciliation available on the company’s web-site and direct users to it.

The 2016 C&DIs mentioned above provide numerous examples of ways in which the SEC considers the presentation of non-GAAP measures to be misleading. The C&DIs divide misleading non-GAAP information disclosures into two broad categories; misleading disclosures that occur 1) if there is an inconsistency between the time periods used to calculate the non-GAAP measure and GAAP measure or 2) if the non-GAAP measure is presented more prominently than the corresponding GAAP measure. Following the issuance of these C&DIs, the SEC received more than 100 comment letters related to the use of non-GAAP measures. EY noted in its 2016 SEC Comments and Trends that the majority of these comment letters focused on issues relating to one of these two categories.

Presentation.

One common form of misleading presentation of non-GAAP measures is exaggerated prominence. Under SEC rules, a non-GAAP measure should not be displayed more prominently than the corresponding GAAP measure.

Headline.

Discussing non-GAAP measures in a headline without discussing the comparable GAAP measure, having the GAAP measure follow the non-GAAP measure in the headline, and placing the non-GAAP measure in bold, italics, or larger print as compared to the typeface for the GAAP measure, are all examples of misleading prominence.

Text.

Likewise, placing non-GAAP measures in bold, italics, or larger print, or using positive adjectives such as “record performance” or “exceptional” to describe the non-GAAP measure without a similar, accurate description of the GAAP measure, constitute misleading prominence.

Table presentation.

Companies should avoid providing a table of non-GAAP earnings measures without a similar table for the comparable GAAP earnings measures, or presenting a non-GAAP table before and more prominently than the similar GAAP table. GAAP and non-GAAP information may be presented in the same table; however, the style of presentation between the GAAP and non-GAAP numbers should be consistent.

Analysis.

Discussing and analyzing the non-GAAP financial measure without a similar discussion and analysis relating to the most comparable GAAP measure is a form of misleading prominence, as is displaying the discussion and analysis of the non-GAAP financial measure more prominently than the comparable GAAP earnings measure.

Income statement.

Companies should not present a complete non-GAAP income statement, either as a stand-alone document or as part of a reconciliation to a GAAP income statement.

Calculation.

Problems related to the calculation of non-GAAP measures occur when non-GAAP financial measures are not calculated consistently for different periods or for similar economic events, or when a company creates its own accounting principles (e.g., revenue and expense recognition) for its non-GAAP financial measures and these principles do not comply with U.S. GAAP.

Lack of consistency.

Consistency can be thought of as reporting similar items—whether they are revenues or expenses—the same (i.e., including or excluding) within a reporting period or over time. Examples include the following:

- Lack of consistency between periods—the inclusion or exclusion of different revenue and expense items in the calculation of non-GAAP earnings varies between periods; for example, recording a gain in one period and excluding the same gain in the next period.

- Lack of consistency relating to similar items—treating similar gains and losses differently for a specific period or in several reporting periods. For example, recording a gain in non-GAAP earnings but excluding a similar expense from the non-GAAP earnings calculation, or recording a gain in one period but excluding a similar loss in a subsequent period.

- Nonrecurring gains—inclusion of non-recurring gains in the non-GAAP earnings calculation.

“Creative” accounting principles.

This relates to companies creating unique accounting principles to recognize revenues or expenses, such as the following:

- Exclusion of operating expenses—non-GAAP measures that exclude normal, recurring operating expenses.

- Revenue recognition—reporting a non-GAAP earnings metric that accelerates revenue recognition, as compared to GAAP revenue recognition.

- Expense recognition—reporting a non-GAAP earnings metric that decelerates expense recognition, as compared to GAAP expense recognition.

Per-share basis.

Companies are only allowed to present non-GAAP performance measures on a per-share basis; non-GAAP liquidity measures may not be presented on a per-share basis. The SEC determines whether a non-GAAP measure is a performance or a liquidity measure and will not rely on the company’s characterization. Free cash flow, earnings before interest and taxes (EBIT), and earnings before interest, taxes, depreciation, and amortization (EBITDA) should not be presented on a per-share basis.

If management believes that publicly disclosing a non-GAAP measure will be beneficial to investors, it must explain why the non-GAAP number provides a better performance measure than the GAAP number.

Forward-looking measures.

If a company decides to present forward-looking non-GAAP financial measures for which the corresponding GAAP financial measure has not been determined, the company must state that the GAAP reconciliation is unavailable without unreasonable effort, provide reconciling items that are available, discuss the significance of the reconciling items that are unavailable, and ensure that the measures are not displayed in a more significant or prominent manner.

Net of tax.

Companies should not present non-GAAP financial measures as “net of tax.” Instead, companies must calculate and disclose the tax effect of the reconciling item along with its effect on the non-GAAP earnings measure.

The SEC Is Watching

When they first began to be used, non-GAAP earnings were presented in accordance with GAAP but would highlight a material change in the operating structure or accounting method of the company. In the late 1990s, non-GAAP financial measures evolved into a way for companies to exclude certain nonrecurring revenues or expenses from the GAAP-based earnings number. The motive for this adjustment was to eliminate these revenues or expenses to provide investors with a greater degree of understanding of the company’s ongoing core business; however, a lack of guidance gave companies the opportunity to report potentially misleading non-GAAP financial measures.

The SEC has become proactive in providing guidance for and monitoring of the use of non-GAAP financial measures after companies have presented potentially misleading non-GAAP measures. It is currently focusing on the comparability of non-GAAP financial measures across periods and the use of creative accounting principles. Financial reporting executives and CPAs are encouraged to continue to monitor the SEC and IASB for future guidance relating to non-GAAP financial measures.

Seanna Asper, CPA is a PhD student at the Culverhouse School of Accountancy at the University of Alabama, Tuscaloosa, Ala.

Chris McCoy, CPA is an assistant professor at the College of William and Mary, Williamsburg, Va.

Gary K. Taylor, PhD is an associate professor, Pricewaterhouse Coopers Faculty Fellow, and C&BA Endowed Professor at the Culverhouse School of Accountancy, University of Alabama.