by CPA Journal | Oct 4, 2017 | Articles, ASC 842, IFRS 16, IFRS Accounting, Lease Accounting

A fter a nearly 10-year collaboration to develop a converged standard on leasing, on Jan. 13, 2016, the IASB issued IFRS 16, Leases, and on Feb. 25, 2016, FASB issued Accounting Standards Update (ASU) 2016-02, Leases—Topic 842. The two standards differ...

by CPA Journal | Sep 27, 2017 | Articles, ASC 842, Lease Accounting, US GAAP Accounting

Summary provided by MaterialAccounting.com: This article explains how to account for leases under FASB’s new accounting standard, ASC 842. In contrast to the lessee model, the lessor model under FASB’s new lease accounting standard has three different...

by CPA Journal | Sep 7, 2017 | Articles, ASC 840, ASC 842, Lease Accounting, US GAAP Accounting

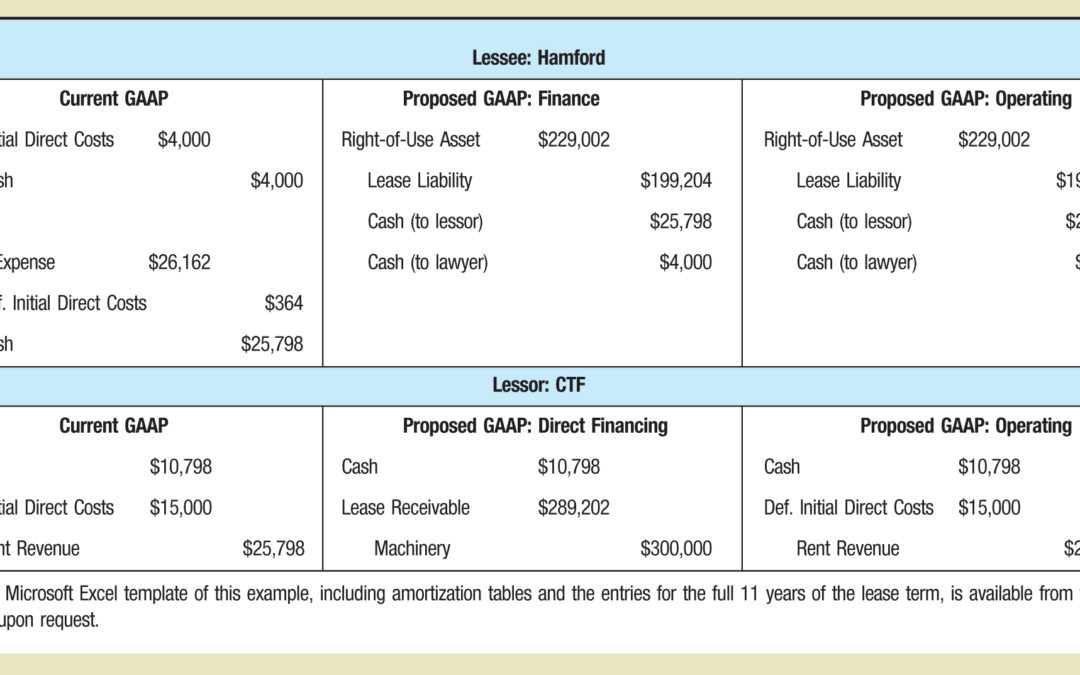

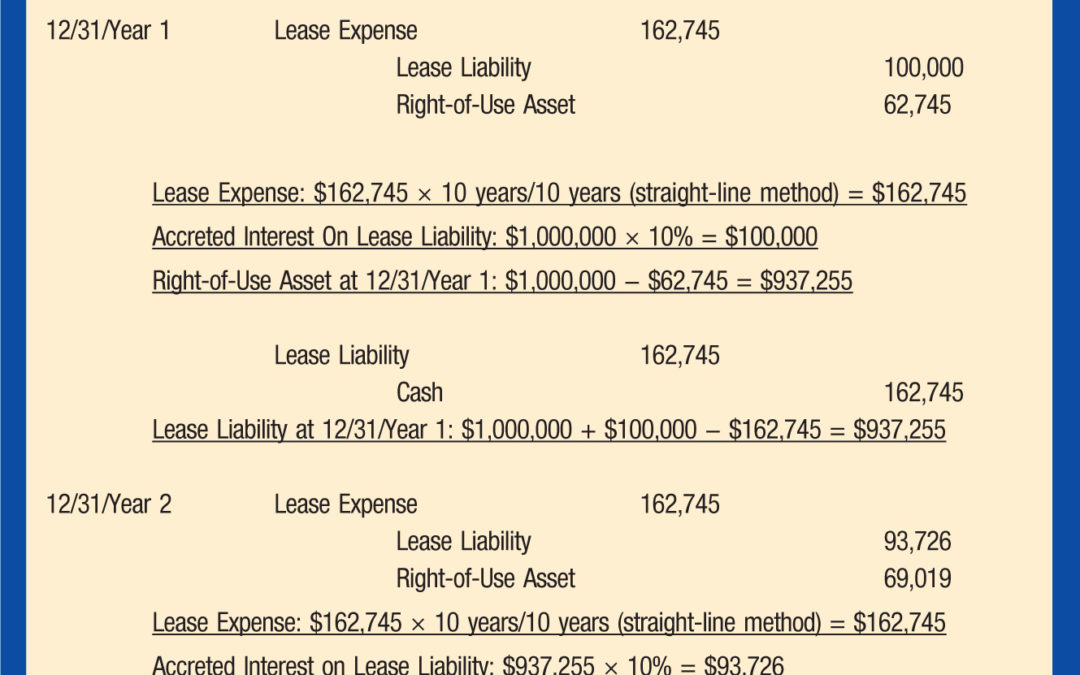

In Brief FASB’s long-debated exposure draft of a new standard on accounting for leases has raised the possibility that almost all leases will need to be capitalized in the near future. Although some of the methods in the proposed standard are similar to those used...

by CPA Journal | Aug 28, 2017 | ASC 842, Lease Accounting, Revenue Recognition, Uncategorized, US GAAP Accounting

The panel began with a discussion of the new standard for revenue recognition and the process for implementing it. Siegel highlighted some of the more prominent changes, such as moving the recognition of collectability to the beginning of the contract process and...

by CPA Journal | Aug 23, 2017 | Articles, ASC 606, ASC 842, Lease Accounting, Revenue Recognition, US GAAP Accounting

In Brief The new lease accounting standard, released by FASB in early 2016, represents one of the largest and most impactful reporting changes to accounting principles in decades. The standard itself is voluminous, and digesting it will be a major task for companies,...